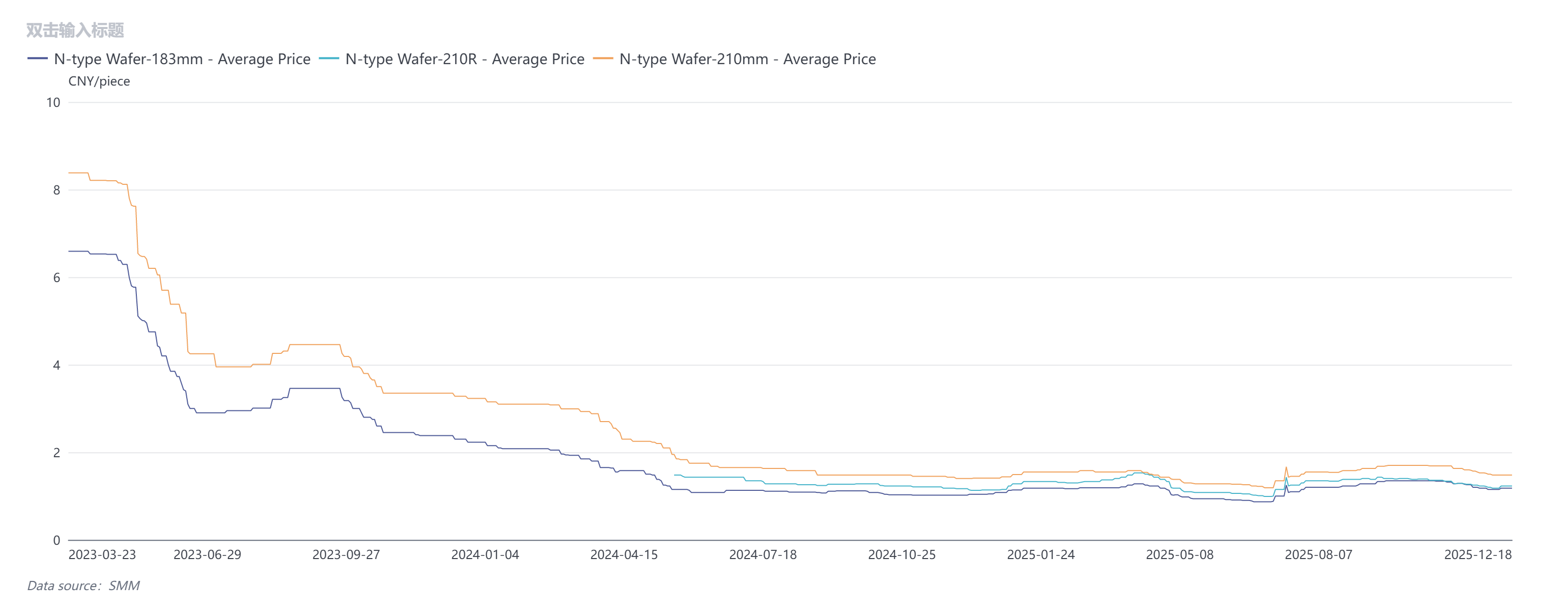

In December, overall wafer prices first fell and then rose, with N-type 183 wafer prices at 1.15–1.2 yuan/piece, 210R wafer offers at 1.2–1.25 yuan/piece, and 210mm wafer offers at 1.45–1.5 yuan/piece. Notably, the high price of 210R wafers remains subject to back-and-forth negotiations between upstream and downstream. Given the current situation, it is unlikely that cell enterprises will accept wafer price increases at the cost of expanding losses. The recent price fluctuations were mainly driven by upstream sentiment, while the reality and expectations of weakening demand have not changed. Going forward, close attention should be paid to the results of the Self-Discipline 2.0 association meeting and the extent to which enterprises actually comply.

According to SMM's daily wafer cost, taking the 210R size as an example, the tax-exclusive full cost decreased from 1.408 yuan/piece in October to 1.403 yuan/piece in December, yet the profit margin expanded from -12.03% to -22.41%. Data indicate that during the same period, the proportions of 210R silicon cost, non-silicon cost, and three expenses (selling expenses, administrative expenses and financial expenses) were 49%, 48%, and 3%, respectively, with the ratios remaining largely unchanged. Fluctuations in the prices of auxiliary materials such as crucibles and gases were negligible. Therefore, the core reason for the significant profit decline lies in the substantial drop in wafer selling prices. As can also be seen from the chart above, the tax-inclusive selling price of 210R wafers fell from 1.4 yuan/piece to 1.23 yuan/piece, a decrease of 12.1%. Based on market surveys, SMM expects that the cost of 210R wafers in December will have some downside room due to lower crucible prices, and there is potential for profit recovery. However, it remains to be seen whether the current price increases will be accepted by cell enterprises.

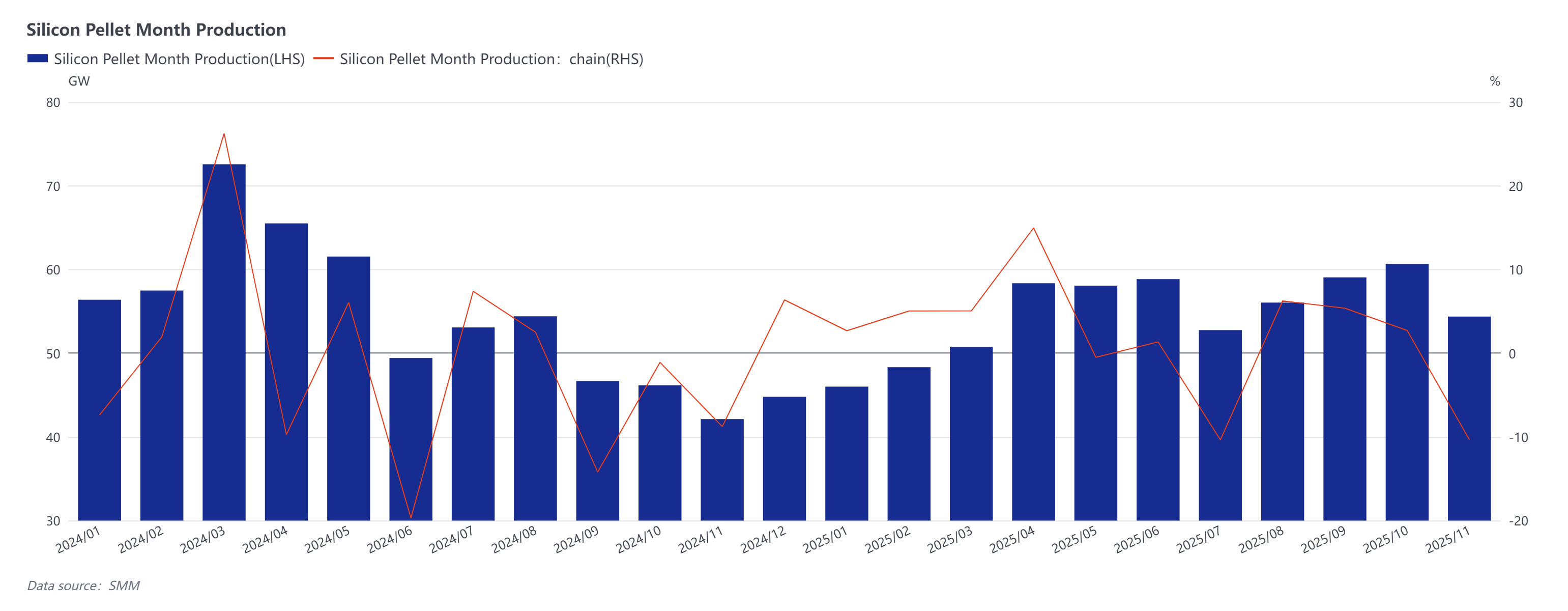

According to SMM statistics, wafer production in December is expected to be 45.7 GW, down 15.95% MoM. The actual production schedule change should be relatively small. At the beginning of the month, the rapid decline in wafer prices led several enterprises to cut production more than expected. However, by mid-December, three enterprises gradually increased production to varying degrees, with the increment offsetting the previous cuts, keeping the overall level in line with expectations. Based on supply-demand balance calculations, cell demand exceeds supply by approximately 2 GW. However, considering the recent sharp rise in silver paste prices, which has expanded cell losses, enterprises are forced to implement significant production cuts. Therefore, the actual production schedule may be slightly lower than expected, resulting in a tight supply-demand balance or slight destocking in December.

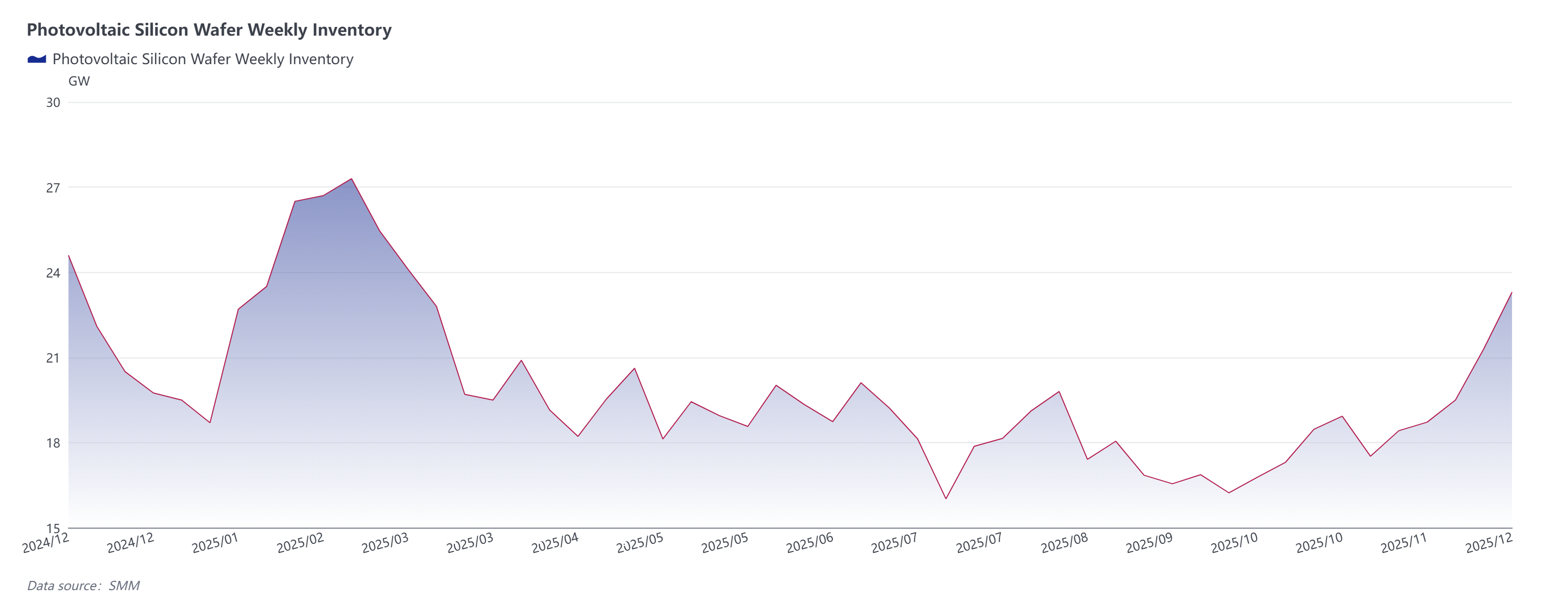

According to the latest SMM statistics, current upstream wafer finished product inventories amount to approximately 23.3 GW, while downstream raw material inventories stand at about 7 GW, bringing the total wafer inventory to over 30 GW, which is close to a reasonable level. Notably, external toll processing of wafers in December also reached nearly 8,000 mt. Except for two toll processing volumes of around 1,000 mt each that were halted, the remaining reductions were not significant. This portion of volume affects downstream raw material inventories, slowing down the digestion rate of these inventories.

Based on the above data, if polysilicon prices hold steady without dropping before the Chinese New Year, then wafer prices have already bottomed out. As for a rebound driven by market maneuvering, we believe it is quite difficult, especially against the backdrop where cell enterprises are already facing expanded losses due to rising silver paste costs. Currently, multiple upstream segments are attempting to force end-users to accept module price increases by raising prices. However, central state-owned enterprises prioritize yield when procuring modules, and yield is strongly correlated with electricity prices but weakly correlated with module prices. Therefore, these are fundamentally two separate industries; any solution would require adjusting the internal structure of the power system. The consolidation of PV capacity must still be premised on marketization. A market order already exists, and any intervention disrupts market expectations. We observe that high upstream prices are turning speculative demand into speculative supply. The three key metrics—leverage, inventory, and capacity—have not declined; instead, some indicators show an upward trend. This is the reality.

Based on the above data, if polysilicon prices hold steady without dropping before the Chinese New Year, then wafer prices have already bottomed out. As for a rebound driven by market maneuvering, we believe it is quite difficult, especially against the backdrop where cell enterprises are already facing expanded losses due to rising silver paste costs. Currently, multiple upstream segments are attempting to force end-users to accept module price increases by raising prices. However, central state-owned enterprises prioritize yield when procuring modules, and yield is strongly correlated with electricity prices but weakly correlated with module prices. Therefore, these are fundamentally two separate industries; any solution would require adjusting the internal structure of the power system. The consolidation of PV capacity must still be premised on marketization. A market order already exists, and any intervention disrupts market expectations. We observe that high upstream prices are turning speculative demand into speculative supply. The three key metrics—leverage, inventory, and capacity—have not declined; instead, some indicators show an upward trend. This is the reality.

We believe that high-quality PV enterprises should still adhere to high-quality development as a premise, integrate with capital to accelerate transformation, engage in differentiated competition rather than collectively cutting production. They should go global by building capacity through cooperation, abandoning the low-price market-grabbing model in favor of partnering with local enterprises to establish factories, accelerating self-sufficiency in Southeast Asian capacity, supporting influence along the Belt and Road, and expanding the global PV footprint around multiple hubs.

![Brief Review of the Spot Market and China Inventory (April 2, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/PeWqW20251217171735.jpg)

![Brief Review of Silver Market Prices and Expectations (April 2, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/nQsOk20251217171736.jpg)

![[SMM PV News] Abu Dhabi Expands Solar Policy to Residential Sector](https://imgqn.smm.cn/usercenter/HfeeS20251217171739.jpg)